26 Jan FIRPTA Affecting Transactions

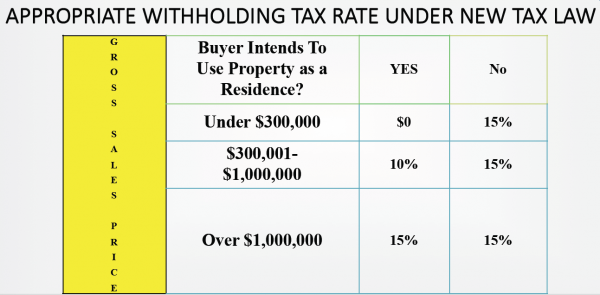

The Foreign Investment in Property Tax Act (FIRPTA) is a certificate of non-foreign status. FIRPTA addresses the disposition of U.S. real property interest by a foreign person. Section 1445 of the Internal Revenue Code requires that all transferees (buyers) of real property owned by a foreign person withhold and pay to the IRS up to 15% of the amount realized on the sale.

The Foreign Investment in Property Tax Act (FIRPTA) is a certificate of non-foreign status. FIRPTA addresses the disposition of U.S. real property interest by a foreign person. Section 1445 of the Internal Revenue Code requires that all transferees (buyers) of real property owned by a foreign person withhold and pay to the IRS up to 15% of the amount realized on the sale.

When dealing with a foreign seller, at the very beginning, agents should be confirming if the seller is a foreign seller or not. If he is a foreign seller (non-resident alien) and does not have an individual tax payer identification number (ITIN), then the agent should recommend he seek the assistance of his CPA in order to apply to the IRS for his ITIN and help him through the paperwork.

Who is a non-resident alien? A non-U.S. citizen who does not pass the green card test or the substantial presence test is considered a “non-resident alien.” If a non-citizen currently has a valid green card, he would pass the green card test and would be classified as a resident alien.

U.S. Real property interests include: Interest in a parcel or parcels of real property.

The IRS definition of an agent: Any person who represents the transferor (seller) or transferee (buyer) in any negotiation with another person (or another person’s agent relating to the transaction in the settling of the transaction).

Liability of agents: If the transferee (buyer) or other withholding agent receives a certification of non-foreign status and the agent knows that the document is false, the agent must provide notice to the transferee (buyer) or other withholding agent. If the notice is not provided, the agent will be liable for the tax that should have been withheld but only to the extent of the agent’s compensation from the transaction.